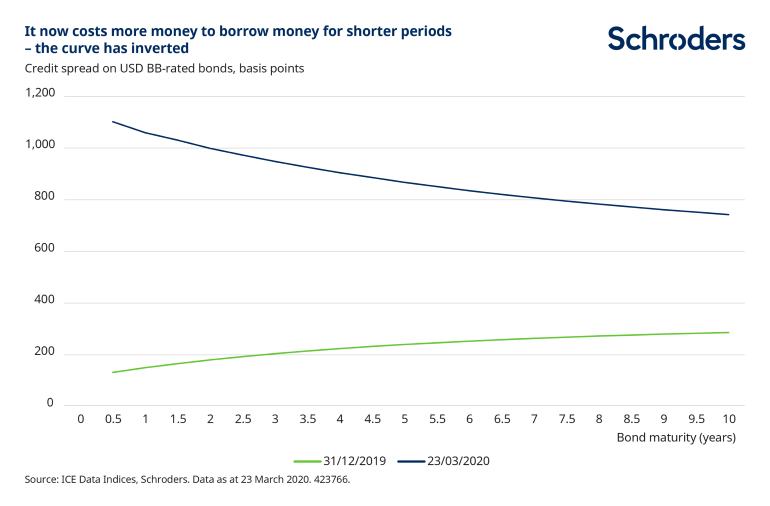

The disruption and risk aversion resulting from the coronavirus pandemic has caused any number of extreme and unusual events across financial markets. Among these we now have an inversion of the corporate bond credit spread curve, as the bond market sees a significant risk of companies facing near-term financial pressures amid reduced economic activity.

What’s happening with the credit spread curve?

The normal state of affairs in corporate bond markets is that the longer a company borrows money for, the higher the credit spread it must pay. This is the margin it has to pay in excess of government yields, and a measure of how risky the market sees the borrower. This relationship between bond maturity and credit spread is fairly typical across bonds of all credit ratings.

One reason why this happens is that the longer the term to maturity of a bond or loan, the more uncertain it is that it will ultimately be able to repay the debt. In normal circumstances, it might be relatively easy to take a view on whether a company will still be financially viable, and able to repay its debt, over a year or two. But 10 years from now? That is a lot harder.

This normal relationship has recently been upended, as the chart shows. For many companies it now costs more to borrow money for shorter periods than longer. This is an indication of just how risky the market now sees near-term conditions for businesses. Essentially, the market is saying it sees a significantly increased risk that some companies may not be able to afford the large principal payment which comes when a bond reaches its maturity, or be able to refinance the debt with new borrowings.

While decidedly unusual, it also does makes sense. Coronavirus has introduced unprecedented social and economic conditions. With whole countries in lockdown, reduced economic activity, particularly consumption, will mean reduced sales and revenues for companies. This will ultimately put a strain on company cash flows, in some cases reducing their ability to repay debt, certainly in the near-term. Such is the impact of coronavirus and the visibility of short-term risk.

By the same token, there is some sense to the fact that credit spreads on longer term loans are lower than shorter dated ones. It is reasonable to suppose the world economy will be in a happier state five, seven or 10 years from now, meaning there would be less risk of a company being unable to repay or refinance their debt when it reaches maturity.

How much of a warning sign is this?

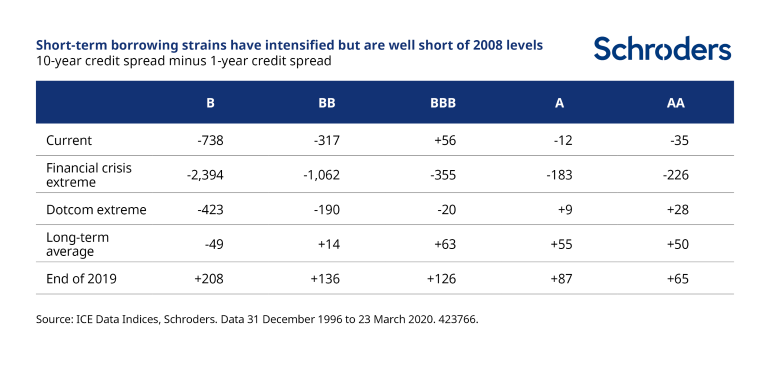

This is a clear indication that the market is expecting some companies to run into near term funding difficulties. The riskiest borrowers, those with a CCC-credit rating, are most exposed. They currently have to pay a credit spread of 25.4% to borrow for five years but, for loans of only one year, that figure would be 42.2%.

However, it is not just risky borrowers who are being affected. Since Friday 20 March 2020, it has also been the case for safer, investment grade rated borrowers. It now costs A-rated companies 0.1% more in credit spread terms to borrow for one year compared with 10-years. Although this is only a small premium, the only other time this has occurred in the past 23 years (the period over which we have good data on credit spreads) was during the financial crisis. It happened to BBB-rated borrowers (the lowest investment grade rating) following the Dotcom crash, but not higher rated A and AA-rated borrowers. This is a highly unusual state of affairs, indicative of the strains on financial markets and companies.

One saving grace is that the extent to which short term borrowing costs exceed longer term costs is nowhere near as pronounced as it was in 2008. The current 317 basis point difference between 1-year and 10-year BB credit spreads is well short of the over 1,000 basis point difference that it reached in November 2008. The strains on higher rated borrowers are also relatively muted compared with 2008, at least for the time being.

This can be interpreted both positively and negatively. The negative interpretation is that near term risks are exceptionally high in view of the much deteriorated economic outlook and that the strains in corporate bond markets could get even worse.

Our economists are predicting a severe recession in 2020 and the worst year for economic activity since the 1930s. Historical experience suggests shorter term borrowing costs could rise much further. Higher rated borrowers, who have so far been relatively shielded from this pressure, could also become more harshly affected.

The positive interpretation is that the increase in short term borrowing costs could have been a lot worse. The fact that it hasn’t been, could be seen as a vote of confidence in the unprecedented response from governments and central banks, with government guarantees of loans, liquidity assistance and deferral of tax payments.

We hope it is the latter but we should not be blind to the possibility it is the former. In this time of such uncertainty, awareness of the risks is one of the best tools available to investors. Developments in the shape of the credit spread curve can be a guide as to which outcome looks most likely. Investors should add this indicator to their toolkit as a way to identify signs of stress in funding markets. It may well provide insight into which industries or companies are particularly vulnerable.

Should default risk be contained, by policy action and/or the coronavirus easing more quickly than expected, then some of the current credit spreads may turn out to be a buying opportunity. Of course, that is unknown today. Only by robust analysis of balance sheets is it possible to identify those companies which are best placed to weather the storm. It is not a time for indiscriminate risk taking.